One of the most difficult decisions retirees and pre-retirees face is how to grow their retirement savings without exposing themselves to excessive market risk. Many investors spend decades accumulating wealth through equities and mutual funds, but the transition from accumulation to income introduces a different set of challenges.

The question becomes less about maximizing returns and more about preserving capital, generating reliable income, and protecting savings from market downturns.

Two commonly discussed investment approaches for retirement portfolios are mutual funds and fixed indexed annuities (FIAs). Each offers distinct advantages and trade-offs. Mutual funds provide access to market growth and diversified investment strategies, while fixed indexed annuities are designed to protect principal while offering limited participation in market gains.

Understanding how these strategies differ—and how they interact with retirement risks such as sequence of returns risk—can help retirees build a more resilient financial plan.

Understanding Mutual Funds in Retirement

Mutual funds remain one of the most widely used investment vehicles for retirement savings. A mutual fund pools money from multiple investors and invests that capital in a diversified portfolio of assets such as stocks, bonds, or other securities.

The primary advantage of mutual funds is growth potential. Equity-based mutual funds historically offer higher long-term returns than most conservative investments.

For retirees who remain invested in the stock market, mutual funds can continue to generate capital appreciation and income through dividends.

Some key benefits of mutual funds include:

Diversification across many securities

Professional portfolio management

High liquidity and accessibility

Potential for long-term market growth

However, mutual funds also expose investors to market volatility. During major market downturns, mutual fund values can decline significantly.

For investors still working and contributing to retirement accounts, market declines may be manageable because they have time to recover. But for retirees drawing income from their portfolios, market downturns can have more serious consequences.

This is where other strategies, such as fixed indexed annuities, may be considered.

What Are Fixed Indexed Annuities?

A fixed indexed annuity (FIA) is an insurance product designed to provide growth linked to a market index while protecting the investor’s principal from losses.

Unlike mutual funds, FIAs do not invest directly in the stock market. Instead, the insurance company credits interest based on the performance of a specific index, such as the S&P 500.

The key feature that distinguishes fixed indexed annuities is the downside protection mechanism.

Most FIAs include a floor of 0%, meaning that if the underlying index performs negatively during a contract period, the annuity does not lose value due to market declines.

This floor protects the investor’s principal from market losses.

However, this protection comes with a trade-off.

While the downside is limited, the upside is also restricted through mechanisms such as caps, participation rates, or spreads.

For example, if an annuity has an annual cap of 6%, and the index increases by 10%, the annuity may only credit the account with a 6% return.

The Trade-Off: Growth vs Protection

When comparing fixed indexed annuities and mutual funds, the fundamental trade-off becomes clear.

Mutual funds offer unlimited upside potential because they participate directly in market performance. If the stock market grows significantly over a long period, mutual fund investors benefit fully from that growth.

However, mutual funds also carry the risk of market downturns.

Fixed indexed annuities offer downside protection, ensuring that investors do not lose money due to negative market performance. But this protection comes with capped gains that limit long-term growth potential.

In simplified terms:

Mutual funds prioritize growth potential.

Fixed indexed annuities prioritize principal protection.

Neither strategy is universally superior. The appropriate choice often depends on an investor’s time horizon, income needs, and tolerance for risk.

Sequence of Returns Risk

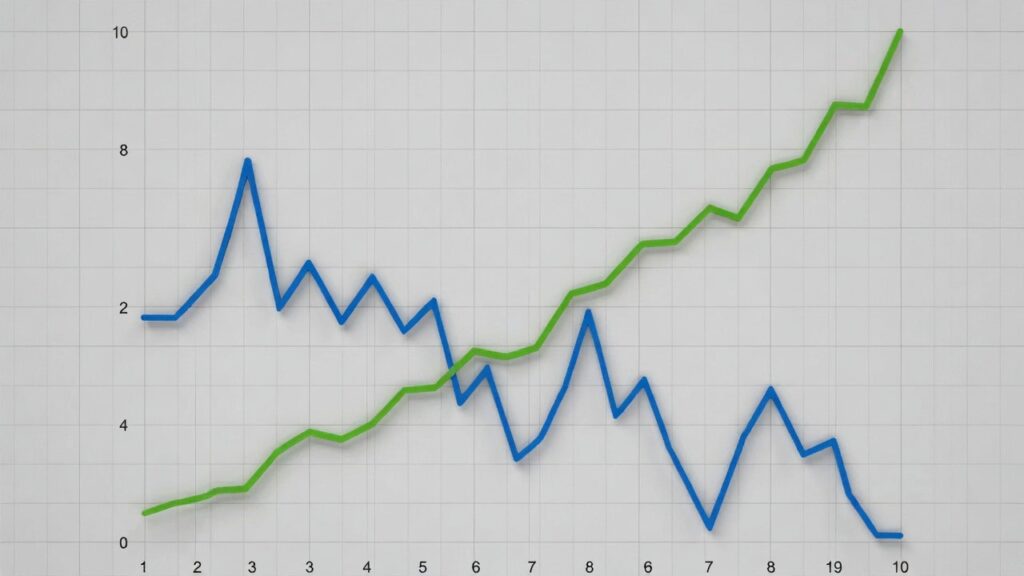

One of the most important risks facing retirees is something known as sequence of returns risk.

Sequence risk occurs when market losses happen early in retirement, especially during the years when an investor begins withdrawing funds from their portfolio.

Even if long-term average returns remain strong, early losses combined with withdrawals can significantly reduce the longevity of retirement savings.

For example, imagine two retirees with identical portfolios earning the same average return over 20 years.

If one retiree experiences negative market returns during the first few years of retirement, while the other experiences those losses later, the first retiree’s portfolio may be depleted much faster.

This occurs because withdrawals during a downturn force the investor to sell assets at depressed prices, locking in losses.

Sequence risk is a major reason why many retirees seek strategies that provide stability or guaranteed income during market downturns.

Guaranteed Lifetime Income

Another key feature often associated with fixed indexed annuities is the ability to convert savings into guaranteed lifetime income.

Many FIAs offer optional income riders that allow the policyholder to receive income payments that continue for the rest of their life, regardless of how long they live.

This feature can help address longevity risk, the possibility that retirees may outlive their savings.

For retirees concerned about creating a reliable income stream, annuities can provide a level of certainty that market-based investments cannot guarantee.

However, income riders often come with additional fees and contract terms that should be carefully reviewed.

Liquidity and Flexibility Considerations

One area where mutual funds have a clear advantage is liquidity.

Mutual funds can generally be bought or sold quickly without long-term contractual commitments.

Fixed indexed annuities, by contrast, are long-term insurance contracts.

Many FIAs include surrender periods, during which withdrawing funds beyond certain limits may result in surrender charges.

These surrender periods often last between five and ten years depending on the product.

For investors who require flexibility or frequent access to funds, mutual funds may be more suitable.

Fees and Cost Structures

The cost structure of these two strategies also differs.

Mutual funds typically charge expense ratios and management fees, which vary depending on whether the fund is actively managed or indexed.

Fixed indexed annuities may include:

Administrative fees

Optional rider fees

Insurance-related costs

While some FIAs advertise low direct fees, the cost of caps or participation limits is often embedded in the product structure.

Understanding the full cost of each strategy is essential when comparing long-term outcomes.

Building a Balanced Retirement Strategy

Many retirement plans incorporate both market-based investments and protected income strategies.

For example, a retiree may allocate a portion of their portfolio to mutual funds for long-term growth while placing another portion into fixed indexed annuities to provide income stability and downside protection.

This type of diversification can help address both growth needs and risk management concerns.

A balanced retirement strategy often focuses on three key objectives:

Preserving capital during market volatility

Generating reliable income

Maintaining growth potential to offset inflation

Achieving these goals typically requires a combination of investment approaches rather than reliance on a single financial product.

Evaluating the Right Strategy for You

Choosing between fixed indexed annuities and mutual funds is not simply a matter of selecting the “better” option.

It is about understanding the trade-offs between growth potential and risk protection, and how those factors align with an individual’s retirement goals.

Younger investors or those with longer time horizons may benefit from the growth potential of mutual funds.

Retirees seeking stability, predictable income, and protection from severe market downturns may find value in the guarantees offered by annuity products.

Ultimately, retirement planning is a highly individualized process that should consider factors such as:

Time horizon

Risk tolerance

Income needs

Tax considerations

Legacy planning goals

Working with a fiduciary advisor can help retirees evaluate these options and design a strategy that balances growth, protection, and income over the long term.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Retirement strategies should always be evaluated with a qualified financial professional who understands your individual financial situation, goals, and risk tolerance.